Quick Thoughts on the 2023 Stress Test Scenarios

Three quick observations

Three quick observations on the scenarios for the 2023 supervisory stress test released this afternoon by the Federal Reserve Board.

Every year the Federal Reserve Board conducts a supervisory stress test of large banking organizations under hypothetical scenarios designed by the Board. The supervisory scenarios are released each February, and results are provided by the end of June. These results are then used to calculate a capital requirement called the stress capital buffer (SCB).

The supervisory scenarios include, at a minimum, the following two elements:

A baseline scenario - i.e., a hypothetical scenario which generally tracks the projections of consensus economic forecasts; and

A severely adversely scenario, which tests banks against an uglier economic environment.

For certain banks, the severely adverse scenario includes two additional components:

A global market shock component designed to stress trading, private equity and other fair-valued positions

A large counterparty default component, which requires banks to assume the default of their largest counterparty (subject to certain exclusions)

The global market shock applies only to banks with significant trading activities,1 a group that this year includes the six U.S. G-SIBs that are not custody banks and the U.S. intermediate holding companies (IHCs) of Barclays, Credit Suisse and Deutsche Bank.

The large counterparty default scenario applies to those same banks, as well as the two U.S. G-SIB custody banks.

The Big New Development: An Additional (Exploratory) Scenario

Last October, former Federal Reserve Board Governor Daniel Tarullo, who served as the Board’s de facto Vice Chair for Supervision until early 2017, gave a speech at the Board’s annual stress testing conference. Tarullo suggested that as the stress testing framework continued to evolve, it might be a good idea for future stress tests to include scenarios in addition to those described above:

The fundamental question is how far out on the tail the regulatory capital requirements are intended to establish resiliency for systemically important banks. At present, the implicit resiliency standard is probably the capacity to remain a viable financial intermediary in the face of a serious, but generally familiar, shock and ensuing consequences. If there were a policy decision to seek greater resiliency to genuine tail events, a promising avenue would be to use multiple non-baseline scenarios – something that was not practically feasible in the early years of CCAR. Although there would obviously still be no guarantee that any of the constructed scenarios would correctly anticipate a future actual stress event, the Board could at least cover several quite different possibilities each year.

In a speech in December 2022, current Vice Chair for Supervision Michael Barr gave a speech that indicated that he too thought that might be an interesting idea.

We are currently evaluating whether the supervisory stress test that is used to set capital requirements for large banks reflects an appropriately wide range of risks. In addition, we are considering the potential for stress testing to be a tool to explore different sources of financial stress and uncover channels for contagion that lead to unanticipated consequences. Using multiple scenarios or adapting the stress test in other ways to better account for the high degree of interconnectedness between banks and other financial entities could allow supervisors and banks to identify those conditions and take action to address them.

An Exploratory Scenario

Today, the Board took its first tentative steps in the direction of the multiple scenario approach floated previously by former Governor Tarullo and Vice Chair for Supervision Barr. Specifically, the Board announced that its 2023 supervisory stress test will subject “the trading books of the largest and most complex banks” to “an additional exploratory market shock.”

Results from this exploratory scenario will not, this year, be used to calculate capital requirements, but “will be used to expand the Board's understanding of the largest banks' resilience” and to “assess the potential of multiple scenarios to capture a wider array of risks in future stress test exercises.”

The Board characterized the key differentiating factor between the supervisory severely adverse scenario and the exploratory scenario as being a less severe recession but one that features greater inflationary pressures.

The purpose of the stress test is to understand a firm’s resilience to a range of severe but plausible events, and the exploratory component furthers that purpose by posing a different set of risks than is probed in this year’s global market shock component.

For instance, while this year’s global market shock is characterized by a severe recession with fading inflation expectations, the exploratory market shock is characterized by a less severe recession with greater inflationary pressures induced by higher inflation expectations. Such differences in scenarios could reveal different losses across banks, depending on the positions held in their portfolios.

The exploratory scenario will apply only to the U.S. G-SIBs.2 Firm-specific results will be released alongside other results near the end of June.

With Apologies, Administrative Law

I poked fun earlier this week at the emerging trend of asserting that the major questions doctrine prohibits [whatever regulatory thing you are opposed to].

I have no idea if that doctrine or any other tenets of U.S. administrative law would materially restrict the Board in future years from testing banks against multiple scenarios that do factor into capital requirements. If pressed, I would guess they would not pose a definitive obstacle. But regardless, here are a few pieces of what may be interesting context.

Dodd-Frank Act

In earlier iterations of the supervisory stress test, the Board tested banks against a baseline scenario, an adverse scenario and a severely adverse scenario. In 2018, the Dodd-Frank Act was amended as shown below.3

Stress Testing Policy Statement

In 2019, the Board amended its Policy Statement on the Scenario Design Framework for Stress Testing to reflect the change made to the Dodd-Frank Act. Consistent with those amendments, the Board’s revised statement says it will now test banks against at least two scenarios, as opposed to at least three.

The Board also, however, consistent with the previous scenario design policy and with the “at least” language retained in the Dodd-Frank Act, reserved the right to include additional scenarios, although it said at the same time that in general it did not expect to do so.

The Board will publish a minimum of two different scenarios, including baseline and severely adverse conditions, for use in stress tests required in the stress test rules. In general, the Board anticipates that it will not issue additional scenarios. Specific circumstances or vulnerabilities that in any given year the Board determines require particular vigilance to ensure the resilience of the banking sector will be captured in the severely adverse scenario. A greater number of scenarios could be needed in some years - for example, because the Board identifies a large number of unrelated and uncorrelated but nonetheless significant risks.

In his 2022 speech, Tarullo lamented this outcome:

Unfortunately, the Dodd-Frank stress test has headed in the opposition direction. In 2018, Congress removed the requirement for an “adverse” scenario to accompany the baseline and severely adverse scenarios. Regrettably, the Fed subsequently dropped the adverse scenario and indicated it was unlikely to use multiple non-baseline scenarios in the future.

I find this lament a little funny given that the 2013 Policy Statement on the Scenario Design Framework for Stress Testing - that is, the one adopted when Governor Tarullo was on the Board - included the exact same language about the Board anticipating it would not issue additional scenarios.4 (Although I guess to be fair that was a statement that three scenarios would generally be good enough, rather than two.)

What Constraints, If Any, Does This Impose?

I find administrative law a bit puzzling at times, especially in the uncertain legal moment we are now in as we wait to see how far the Supreme Court will go in reining in or undermining (delete as appropriate) the regulatory state. So the below is far from an expert opinion.

My preliminary take, though, is that all else equal the Board would be on fairly solid ground under the law to add additional scenarios. Nothing in the Dodd-Frank Act forecloses it, and if Congress actually wanted to stop the Board from doing so, it could have deleted the “at least” language.

I am less sure about how well additional scenarios would fit under the currently existing policy statement on scenario design, however. That policy statement contemplates that multiple scenarios may be appropriate in years where there are a “large number of unrelated and uncorrelated but nonetheless significant risks.” You could make the case that this year is such a year, although the Board’s release today does not try particularly hard to do so and because this is all just exploratory it probably does not need to.

But if the plan is to eventually go to a multiple scenario approach in every year, then I think that requires either changing the policy statement (through notice and comment) or arguing that, in fact, every year is a year that features “a large number of unrelated and uncorrelated but nonetheless significant risks.” That seems like a tougher burden to carry.

Opting In

Banking organizations with $250 billion or more in total assets ($250 billion or more in U.S. IHC assets for foreign banks) are required to participate in the stress test every year. Slightly smaller firms with assets between $100 billion and $250 billion are required to participate only every other year.

This year is an off-year, meaning that most of those smaller banks do not have to participate unless they so choose. Of the banks with a choice,5 only one, RBC US Group Holdings LLC, the entity that holds the Royal Bank of Canada's non-branch U.S. operations, opted in.

At 3.4%, the current 2022-23 SCB for RBC US Group Holdings LLC is not all that high, and is unchanged from the firm’s 2021-22 SCB. (On the other hand, it is higher than the SCB of its Canadian peer, TD, whose SCB is currently equal to the 2.5% floor.)

Still, I suppose that in the capital context every little bit helps, and if RBC can cut down its SCB that might free up some capital it would prefer to have elsewhere.6

Severely Adverse Scenario Changes

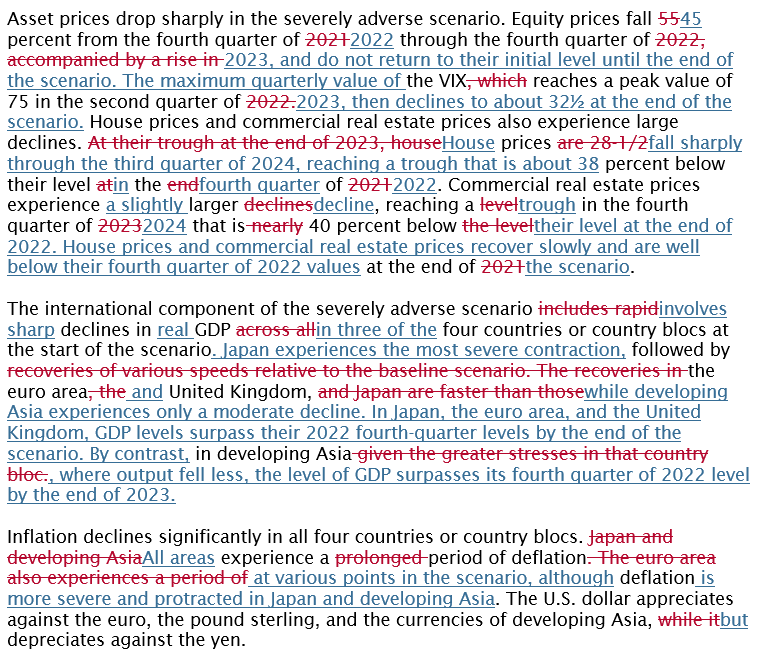

The Board is always very, very clear that its baseline and severely adverse scenarios do not represent economic forecasts. For comparison purposes only, here is a look at the year-over-year differences in the Board’s description of this year’s severely adverse scenario compared to its description of last year’s.

Thanks for reading! Thoughts, challenges, criticisms are always welcome at bankregblog@gmail.com.

Specifically, the GMS component applies to a bank “that is subject to the stress test and that has aggregate trading assets and liabilities of $50 billion or more, or aggregate trading assets and liabilities equal to 10 percent or more of total consolidated assets, and that is not a Category IV firm under the Board’s tailoring framework.”

As in the severely adverse scenario that actually counts, BNY Mellon and State Street “are only required to incorporate an additional counterparty default component into their exploratory market shock component.” The firms “will not be required to apply the exploratory market shock component to calculate mark-to-market losses on their trading or credit valuation adjustments exposures.”

For a full redline comparison showing the changes made to Section 165 of the Dodd-Frank Act by the EGRRCPA, see this 2018 Davis Polk memo.

The 2013 statement read as follows: “The Board will publish a minimum of three different scenarios, including baseline, adverse, and severely adverse conditions, for use in stress tests required in the stress test rules. In general, the Board anticipates that it will not issue additional scenarios. Specific circumstances or vulnerabilities that in any given year the Board determines require particular vigilance to ensure the resilience of the banking sector will be captured in either the adverse or severely adverse scenarios. A greater number of scenarios could be needed in some years—for example, because the Board identifies a large number of unrelated and uncorrelated but nonetheless significant risks.”

Three firms in this category had significant merger applications approved recently and are thus being made to participate this year: “BMO Financial Corp., Citizens Financial Group, Inc., and M&T Bank Corporation are on a two-year stress test cycle; therefore, they were included in last year’s stress test and would normally be included next in 2024. In connection with their recent applications, the Board required these firms to receive a new capital requirement this year based on the 2023 stress test.”

It is also possible RBC just really loves stress testing. The bank also opted in to the 2021 stress test when not required to do so.