Complementary Activities

A Community Bank Sues the Fed

Would it pose a substantial risk to the safety or soundness of banks and the financial system generally for a few home sellers near the Finger Lakes to receive a guarantee on the sale price for their home?

In an order now being challenged in the Second Circuit, the Federal Reserve Board last year concluded that eventually it would, at least when that guarantee is coming from a financial holding company.

The Separation of Banking and Commerce

In the United States a company controlling a bank must generally limit itself to banking and related activities deemed permissible by Congress. There are exceptions, and what falls on the permissible vs. impermissible side of the separation between banking and commerce sometimes varies from firm to firm for reasons not important here. But the essential context for the Federal Reserve Board order that will be discussed in this post is the following.

Under the Bank Holding Company Act a company that controls a “bank” is regulated by the Board as a bank holding company. Section 4(a) of the BHC Act provides that, unless otherwise allowed by Section 4, a bank holding company may not engage in any activities other than banking or managing or controlling banks.

Until 1999, the most important exception to this general prohibition on nonbanking activity was found in Section 4(c)(8). This provision allows bank holding companies to engage in activities that, though not technically banking, have been determined by the Board to be “so closely related to banking as to be a proper incident thereto.” Examples include securities brokerage as agent for customers, or providing financial or investment advice.

In 1999, the Gramm-Leach-Bliley Act amended the BHC Act to allow bank holding companies meeting certain criteria, called financial holding companies, to engage in activities that are “financial in nature or incidental to a financial activity.” A useful, though incomplete, way to think of financial activities is as including all the things previously deemed to be closely related to banking plus investment banking activities like securities underwriting or dealing that previously had been allowed only to a limited extent, if at all.

This aspect of the GLB Act is pretty well known. Some people have strong opinions about it — including occasionally the current President of the United States.

More relevant to this post, the GLB Act also amended the BHC Act to permit a financial holding company to engage in certain non-financial activities, so long as the Board determines the activity is “complementary” to a financial activity and the activity does not pose “a substantial risk to the safety or soundness of depository institutions or the financial system generally.”

Since 1999 the Board has only infrequently considered requests to determine a non-financial activity to be complementary to a financial activity, and the Board’s public orders issued in the 2000s and early 2010s approved only (1) certain activities related to physical commodities, including trading, energy management services and energy tolling,1 and (2) disease management and mail-order pharmacy services.2

The Board later in a 2014 ANPR and other comments indicated it was having second thoughts about aspects of its prior physical commodities complementary activity orders, and in 2016 proposed a rule that would eliminate, narrow or add conditions to some of them.3 The 2016 proposal has never been finalized.

Canandaigua National’s Proposal

Canandaigua National Corporation (Canandaigua National) is the holding company for The Canandaigua National Bank and Trust Company, a community bank with around $5 billion in total assets.

Canandaigua National operates as an FHC. Seeking to leverage that authority, Canandaigua National requested that the Federal Reserve Board make a complementary activity determination with respect to a proposed “cash guarantee mortgage program.” Under the program:4

CNB Mortgage, a subsidiary of the bank, would preapprove a qualifying customer for a residential mortgage loan, with such preapproved buyers providing an earnest money deposit of “at least 15 percent of the purchase price.”

Canandaigua National, as the bank’s holding company, would then offer a guarantee to the seller of the property: if the preapproved buyer was ultimately denied a mortgage “for credit-related or other reasons,”5 the seller would have the right to require Canandaigua National to step into the shoes of the preapproved buyer and “assume all rights and obligations under the contract, subject to the seller’s consent to the assignment.”

If required to perform under the guarantee, Canandaigua National would have the right to subtract from the preapproved buyer’s earnest money deposit “reasonable closing costs and fees to acquire and sell the property, as well as reasonable carrying costs.” But after subtracting such amounts, Canandaigua National would be “obligated to return any remaining funds to the customer, to a maximum of 100 percent of the earnest money deposit.”

Therefore, under its proposal, Canandaigua National could not “use any portion of the earnest money deposit to cover any loss resulting from the resale of the real property at a lower price than the purchase price paid by Canandaigua” and thus would be “exposed to any loss from acquiring and reselling the real property.”

Canandaigua National’s proposal also included proposed commitments and qualitative limits that would have been applicable to the guarantee program. First, Canandaigua National “would guarantee performance only on real estate purchase contracts where the purchase price does not exceed the mortgage preapproval amount authorized by CNB Mortgage.” In addition, purchases of any property “would occur only if the aggregate value of real estate owned under the program after the purchase, as measured by the contracted purchase price for each parcel, would not exceed $5 million at any time.” Finally, Canandaigua National would hold title to the property “for no longer than two years and would seek to dispose of the property promptly.”

The Board’s Order

The Federal Reserve Board announced on October 17, 2025 that it had denied Canandaigua National’s proposal by unanimous vote. In the written order published thereafter,6 the Board concluded that allowing the proposed guarantee as a complementary activity would “pose a substantial risk to the safety or soundness of Canandaigua Bank, depository institutions, and the financial system generally.” Having determined that the proposal must be denied on that basis, the Board chose not to analyze other statutory factors applicable to complementary activity proposals.

Substantial Risk to Safety or Soundness

The Board’s analysis of the substantial risk to safety or soundness factor began with a discussion of provisions of U.S. banking laws that prohibit or otherwise strictly restrict banks and their holding companies from making investments in real property. The order described such restrictions as “intended to ‘keep the capital of the banks flowing in the daily channels of commerce,’ to prevent national banks from direct exposure to real estate, and to forestall the accumulation of significant real estate holdings by national banks.”

Next, the Board noted that it has previously declined to approve certain proposals from bank holding companies that would have involved the bank holding company purchasing, selling, or developing land or real estate, and that Congress has occasionally acted to restrict the Board from approving certain real estate-related activities.

Turning to the specific details of Canandaigua National’s proposal, and after again referencing a “general prohibition on banking organizations investing in real estate,” the Board stated that the proposal “would involve Canandaigua in precisely the type of real estate exposure that the prohibition is intended to prevent.” The Board also argued that, although bank holding companies in some cases may acquire real estate, the activity in which Canandaigua National proposed to engage was much different from the limited activity permitted in those cases. In particular, the order noted that although certain exceptions permit firms to acquire real estate when necessary to “reduce their credit risks,” under Canandaigua National’s proposal the activity involved would have increased the firm’s exposure to credit risk.7

According to the order, Canandaigua National argued that, even if this was the case, any such risks would be appropriately mitigated, including because of Canandaigua National’s (presumably limited) “rate of mortgage denial following preapproval,” its experience disposing of other real estate owned, and the proposed $5 million quantitative limit that Canandaigua National had proposed for the activity.

The Board, however, stated that these mitigants did nothing to change its ultimate conclusion.

To begin, the Board clarified that the question is not, or at least is not only, whether the mitigants would make the activity safe and sound for Canandaigua National. The Board argued that to conduct the analysis in this way would be to “simply focus on the risks that may arise for a particular notificant” and to disregard the statutory mandate to consider risks to “depository institutions or the financial system generally.”

Further, the Board asserted that, in light of its responsibility to consider safety and soundness risks to the financial system generally, there was no possible quantitative limitation on Canandaigua National’s activities that would make this activity safe and sound:

Given the risks discussed above, the Board is unable to determine that Canandaigua’s proposed activity does not pose a substantial risk to the safety and soundness of financial institutions or the financial system generally, regardless of the proposed quantitative limit on the activity.

The Board followed this statement with a brief summary of how “downturns in the market for real estate have caused excess harm to the banking system and financial institutions.” The order cited the 1980s savings and loan crisis, the failure of a “significant number of banks in the northeastern United States … in the early 1990s,” and the “longest and deepest recession in generations” that began to emerge in 2007. The Board contended that allowing FHCs to engage in the activities proposed by Canandaigua National “arguably” would leave FHCs “even more exposed to the types of risks that contributed to these banking system crises” that the order had just summarized.

Therefore, the Board concluded that the safety and soundness factor was inconsistent with approval, and that the proposal must be denied.

Other Statutory Factors

The Board chose not to fully undertake an analysis of whether the benefits from the proposal could reasonably be expected to outweigh the possible adverse effects. The order argued that because the Board had concluded that safety and soundness considerations alone required denial of the proposal, analysis of this other statutory factor was rendered unnecessary.

The Board did, however, include a brief paragraph in which it noted that “certain aspects” of the proposal “raise concerns” even aside from the safety and soundness analysis. In particular, the Board argued that Canandaigua National’s asserted benefits from the proposal would need to be weighed against “the unsound banking practices involved in real estate investment” and “the negative financial impact that could fall on potential customers who lose their earnest money deposit.” The Board then stated that these considerations meant it was “not clear” it would have been able to find in Canandaigua National’s favor on this statutory factor.

Pending Second Circuit Litigation

After the Board’s initial disapproval of the proposal in October, Canandaigua National requested reconsideration. The Board, through its General Counsel acting under delegated authority, denied that request by letter on November 10. The letter stated in relevant part:8

To the extent the Request presents new asserted facts, principally certain information highlighting Canandaigua’s decreasing proportional share in the market for mortgages in the markets which Canandaigua competes, the Request does not provide relevant information that warrants Board reconsideration of its action. These new asserted facts are not material to the Board’s determination.

Canandaigua National then sought review of the Board’s order in the Second Circuit. The Board responded by filing the administrative record as required. An opening brief from Canandaigua National, with lead counsel listed on the docket from the Rochester office of a New York law firm, is currently due by April 21, 2026.

Four Questions

It is rare for the Board to formally issue a public order on a complementary activities request, and rarer still for the Board to formally and publicly deny an application of any kind. Nonetheless, the Board’s Canandaigua National order and the ensuing Second Circuit litigation do not appear to have yet drawn much public notice or comment. The remainder of this post highlights a few questions that may receive more attention as the litigation proceeds.

1. How Did the Board Define “Substantial Risk to Safety or Soundness” In This Context?

When evaluating a proposed complementary activity under Section 4(k)(1)(B) of the BHC Act, the Federal Reserve Board is required to determine whether the activity would “pose a substantial risk to the safety or soundness of depository institutions or the financial system generally.”

Here, the Board concluded that the proposal would not only pose a substantial risk to the safety and soundness of banks or to the financial system generally, as the statute describes, but would in fact pose a substantial risk to the safety and soundness of all of “Canandaigua Bank, depository institutions, and the financial system generally.”9

In the course of reaching this conclusion, the Board argued that safety-and-soundness risks are “considerable” and are “inherent in investing in real estate.” But despite basing its conclusion on safety and soundness, the Board in the order never defined that term, nor did it expressly quantify the degree of risk necessary to rise to a level that is “substantial.”

Is The Board Applying a Material Financial Risk Standard?

This may not have been the Board’s intention, but at least for this blog it was difficult to read the Board’s order without thinking of the separate ongoing debate about how to define “unsafe or unsound” practices under Section 8 of the FDI Act. The FDIC and OCC proposed last year to adopt a definition of this term focused on actions or inactions contrary to generally accepted standards of prudent operation that resulted in, or are likely to result in, “material financial harms” to a bank or to the Deposit Insurance Fund. The Federal Reserve Board also indicated last year that how the Board applies the unsafe or unsound standard “will be changing,” although the Board unlike the FDIC and OCC has not as of the date of this post issued a proposal.

The idea that the question of whether an activity is unsafe or unsound ought to be resolved by looking to whether the activity presents a risk of material financial harm comes to mind here because, as discussed above, Canandaigua National proposed to limit the aggregate value of real estate owned under the guarantee program to no more than $5 million at any time. Based on Canandaigua National’s most recent financial statements, $5 million is equivalent to a quite small percentage of the metrics the Board in previous complementary activity orders has benchmarked the scale of a proposed activity against.10

Even so, the Board here concluded that, regardless of this $5 million limit or any other limits that Canandaigua National might apply, risks to the safety and soundness of Canandaigua National, and to the financial system generally, would be “substantial” for purposes of Section 4(k)(1)(B).

This might suggest that something other than a risk of material financial harm is what made this proposed activity, in the Board’s view, a risk to safety and soundness. Similarly in the portion of the order commenting on the Section 4(j)(2) factors, the Board’s statement that it believes real estate investments necessarily involve “unsound banking practices,” apparently without regard to the nature or extent of such investments, may be in some tension with the idea that an “unsound” practice must be one that implicates a material financial risk.

So what standard is the Board applying here?

One Potential Argument for the Board: This Is Still a Material Financial Risk Standard

Well, maybe the above got a little carried away. The Board still may be able to argue that its ultimate conclusion as to substantial risk to the financial system as a whole is consistent with a standard based on material financial risk.

To get there, the Board might start from the premise that if this proposal was approved then other FHCs would quickly begin to seek to offer their own guarantee programs. This could then give rise to a scenario where hundreds of FHCs are piling into real estate investment at the same time. In that scenario, even if each firm individually is involved in real estate investment in limited amounts, this could pose material financial risks to the system as a whole. This is something the Board might be particularly worried about in the event of a downturn, given interconnectedness between financial institutions and other factors the Board thinks about when evaluating financial stability.

This general type of concern seems to be the implicit argument of the Board order, even if the links in this causal chain are not always connected clearly. For example, a source cited in footnote 29 of the order calls the level of bank participation in real estate markets in the 1980s “aggressive,” and the Board similarly describes as “significant” the lending exposures of a number of northeastern banks in the 1990s. The Board then contends that “arguably” Canandaigua National’s proposal “would leave [FHCs] even more exposed to the types of risks” behind those 1980s and 1990s crises, as well as the one starting in 2007.

The Board’s use of the word “arguably,” without then going on to provide further argument, leaves some work for the reader to do to connect the dots. But if the Board’s conclusion is that approving this proposal would eventually lead to “aggressive” and “significant” risk exposures for FHCs, and for that reason the risk to safety and soundness is substantial, then maybe this is essentially a material financial risk approach after all.

Another Potential Argument for the Board: No, This Is Not a Material Financial Risk Standard … But So What?

There are also other answers the Board might be able to offer in response to a complaint that its conception of safety and soundness under Section 4 of the BHC Act is different from the approach focused on material financial risk that the FDIC and OCC have proposed under Section 8 of the FDI Act.

One answer might be to say that the FDIC and OCC’s whole premise is wrong, and that they are incorrect to believe that unsafe or unsound under Section 8 ought to be understood as embracing a standard based on material financial risk. A few commenters on the FDIC/OCC proposal made this argument.

Maybe more interesting though would be a different type of answer that assumes for the sake of argument that the FDIC/OCC’s proposed interpretation of Section 8 is appropriate, but nevertheless concludes this is not necessarily relevant to the Board’s analysis under the BHC Act. One way to arrive at this view might be by pointing out that the above discussion in this post maybe plays a bit fast and loose with the statutory language. In fact, BHC Act Section 4(k)(1)(B) (“safety or soundness”), BHC Act Section 4(j)(2) (“unsound banking practices”) and FDI Act Section 8 (“unsafe or unsound practice”) all use at least slightly different language, and thus could, and the Board might be able to argue should, be read to mean at least slightly different things.

It is not clear which of the above views, if any of them, is currently held by the Federal Reserve Board, but the Second Circuit litigation may give it the opportunity to explain.

2. Are All the Considerations Discussed in the Order’s Analysis Relevant Under the BHC Act?

Maybe all of this will wind up being academic, but the Board’s choice to leave ambiguous how it is defining and applying Section 4(k)(1)(B)’s safety and soundness standard in this context is made more frustrating by the space the order gives to factors that do not seem obviously relevant to that standard.

A General “Prohibition Against Bank Holding Companies Investing in Real Estate”

For example, the Board at multiple points characterizes Section 4(a)(2) of the BHC Act as a “prohibition against bank holding companies investing in real estate” and ultimately concludes that approving Canandaigua National’s proposal would “would involve Canandaigua in precisely the type of real estate exposure that the prohibition is intended to prevent.”

But even granting the Board its premise that the activity proposed here represents “precisely” what Section 4(a)(2) intends to prohibit,11 does it necessarily follow that whether something is prohibited by Section 4(a)(2) should affect the complementary activities analysis in the first place?

In this order, the Board is making a determination under Section 4(k)(1)(B) of the BHC Act. Section 4(k)(1) provides that the Board is to make such determinations “notwithstanding subsection (a)” of Section 4. This is because, as the Board acknowledges early in the order, the purpose behind adding the complementary activities provision to the BHC Act was to allow the Board to permit, subject to certain safeguards, “an activity that appears to be commercial rather than financial in nature.”

If that is so, isn’t it the case that a complementary activities order by the Board under Section 4(k)(1)(B) will always involve an activity otherwise prohibited by Section 4(a)(2)? If the activity was financial, there would be no need to seek to use complementary authority under Section 4(k)(1)(B) in the first place. And if an activity being otherwise prohibited by Section 4(a)(2) meant that an activity could not be considered complementary, no complementary activity could ever be approved.

Pre-GLB Act Board Orders Under the BHC Act

The Board also in the course of its safety and soundness discussion observes that it has previously “determined in 1972 that land development activity was not an activity closely related to banking” and has held in 1995 that “real estate brokerage activities are not permissible under the BHC Act.”

What relevance do orders like these, issued in decades past and before Section 4(k) was added to the BHC Act in 1999, have in determining the activities financial holding companies should now be allowed to conduct?

The Board has considered this question before. 25 years ago, it suggested the answer was very little:

Second, the [National Association of Realtors] suggests that it would be inappropriate for the Board now to permit FHCs to provide real estate brokerage services because the Board prohibited bank holding companies from acting as a real estate broker in 1972. As noted above, the Board’s 1972 decision on real estate brokerage was made pursuant to the former “closely related to banking” standard; the GLB Act now authorizes the Board to approve any activity that is “financial in nature” or “incidental to a financial activity.” The plain meaning of and legislative history behind the “financial” and “incidental to financial” standards suggest that Congress intended the new standards to be significantly broader than the old “closely related to banking” test. Furthermore, the financial services environment has changed significantly in the past 30 years, and what may have been an inappropriate activity for bank holding companies in the early 1970s may be appropriate for the diversified FHCs of the early 21st century.

The Board never finalized the proposal from which this quote comes, so maybe it is a little unfair for this blog to bring it up now. But even if the Board’s previous reasoning is not legally binding on it, isn’t it at least a little funny to see the Board in the above quote from 2000 dismiss the 1972 order as reflecting the financial services environment of thirty years before, only for the Board to then in 2025, more than fifty years later, reach for the 1972 order as a source of support?

Maybe sensing the potential problem with attempting to give weight to an old order issued under a different subsection of the BHC Act, the Board in the Canandaigua National order goes on to acknowledge that after the 1972 and 1995 orders were issued, the GLB Act expanded the powers of FHCs. The Board then argues, however, that the most important thing about the GLB Act in this specific context is that it did “not amend[] the prohibition against bank holding companies investing in real estate” (i.e., the Board’s preferred way to describe, for purposes of this order, Section 4(a)(2) of the BHC Act).

But this argument, too, may not get the Board very far. It is true that Section 4(a)(2) itself was not amended, but the GLB Act did add the Section 4(k)(1) provision allowing the Board to make complementary activity determinations “notwithstanding Section 4(a).” So even if Congress did not touch Section 4(a)(2) specifically, it did contemplate that Section 4(a)(2)’s application could be narrowed if the Board otherwise found favorably on the statutory factors.

The Financial Services and General Government Appropriations Act, 2009

As a final example, consider the Board’s discussion, again in the middle of what is framed as a safety and soundness analysis, of an appropriations bill passed by Congress in 2009. A provision of that appropriations bill, still in force today, prohibits the Board from determining that “real estate brokerage activity or real estate management activity” is permitted under Section 4(k), whether as a financial activity, an incidental activity, or a complementary activity.

Immediately after noting that this law exists, the Board seems to betray some doubts about its choice to discuss that law in this order, quickly clarifying in a footnote that it “does not believe that [Canandaigua National’s] proposed cash guarantee mortgage program constitutes real estate brokerage activity or real estate management activity.” In other words, the 2009 law does not affect the Board’s ability to approve Canandaigua National’s proposal.

Beyond the issue the Board identifies, bringing this law up in the context of this order may be unhelpful for another reason. Under some approaches to statutory interpretation, Congress’s action (and inaction) may work against the conclusion the Board wishes to reach. The argument would go: Congress evidently knew how to prohibit specific types of real estate activities from being authorized under Section 4(k)(1), and then, having that knowledge, and having seen a decade of how the Board had been applying the Section 4(k)(1) authority, deliberately chose to leave untouched the Board’s ability to approve activities like those reflected in Canandaigua National’s proposal. Put differently, if Congress in fact wanted guarantees like those proposed by Canandaigua National to be prohibited for FHCs, why hasn’t Congress acted to ban FHCs from offering them, in the same way it acted in the 2009 appropriations law to prohibit FHCs from engaging in real estate brokerage or real estate management?12

— — — —

Nothing in the above discussion should be taken for an argument that the Board is obligated generally to approve every request received under Section 4(k)(1)(B), or that the Board was obligated specifically to approve this one. Of course not.

But if it is the case that, as explained in the Board’s early complementary activity determinations, “the only limitations”13 on this authority are that the activity be complementary, that the risks to safety and soundness not be substantial, and that the public benefits reasonably are expected to outweigh the potential adverse effects, then where does the Board see the considerations discussed above as fitting in?

3. Is the Board’s Approach to Limits and Weighing of Benefits and Risk Consistent with Previous Complementary Activity Orders?

As mentioned earlier in this post, although it has issued few orders with respect to complementary activities overall, one place where the Board’s complementary activities determinations had at one time been relatively more active was in relation to physical commodities. Although the Board never says so explicitly, there are at least two ways its analysis in the Canandaigua National order could be read as breaking with aspects of the analysis adopted in those prior orders.

Quantitative Limitations and the Financial System as a Whole

The Canandaigua National order argues that limitations are “relevant” to the Board’s analysis, but not necessarily dispositive as to “broader safety-and-soundness risks,” given the statute’s requirement that the Board consider the “financial system generally.”

On its own, this seems fair enough, both as a description of what the statute requires and as practical matter. It is not impossible to imagine a set of scenarios where proposed quantitative limits might make an activity safe for a given firm, without being sufficient to make the activity safe for the financial system as a whole, assuming all firms were to engage in the activity to the same extent.

Where the order might be on shakier ground, however, is in its attempt to frame this approach to quantitative limits as following naturally from the Board’s analysis in prior orders.

The Board supports its statement in the Canandaigua National order that limitations are “relevant” with a citation to its 2007 Wellpoint order. That 2007 order does feature a discussion of quantitative limits, but the discussion there is much different than the discussion here. The Wellpoint order gives the impression that firm-specific limitations are not merely relevant to the safety and soundness analysis but are the beginning and end of it. The analysis is entirely focused on the limits on Wellpoint’s own activities and the impact of those limits on Wellpoint, without an explicit separate analysis of the “broader safety-and-soundness risks” to the financial system generally that the Board in this Canandaigua National order now says it always “must take into account.”

The Wellpoint order did not involve physical commodities and maybe is distinguishable as arising in an unusual context, but the Board’s physical commodities complementary activity orders feature the same analytical approach. Firm-specific limits are described in many different orders as “critical to the determination” of safety and soundness, and the analysis consistently focuses on the individual firm, including its “policies and procedures for managing and controlling the risks,” without separate analysis focused on the financial system generally.

Of course, even if not stated explicitly in these older orders, conditions can be “critical” to a determination while not on their own being sufficient, so the Board may be able to argue that even if the discussion in the Canandaigua National order is framed differently, in substance this does not actually represent a dramatic analytical break from prior orders.

Still, it would have been interesting – and perhaps challenging – for the Board to have more clearly explained why in this real estate context no set of limitations could ever be sufficient to address safety and soundness concerns, even though in many prior orders limitations have been sufficient to mitigate the risks raised by physical commodities activities. Particularly given that the Board has previously assessed the risks of those physical commodities activities as “unique in type, scope and size.”14

Section 4(j)(2) Balancing

Section 4(j)(2) of the BHC Act requires the Board to balance reasonably expected benefits against possible adverse effects. In this context, the Board’s physical commodities complementary activity orders have recognized various potential benefits:15

facilitating customers’ desire to receive “a full range of commodity-related services,” and the firm’s desire to “transact more efficiently with” those customers;

allowing the firm to “acquire more experience in the markets for physical commodities”;

enhancing the firm’s “understanding of physical commodity and derivatives markets”;

enabling the firm to “serve as an effective competitor” with “non-BHC participants” in the relevant market; and

increasing the “profitability of [the firm’s] existing BHC-permissible” activities.

The orders have then gone on to find that these potential benefits outweigh possible adverse effects, with the latter usually not specified in detail.

In Canandaigua National’s case, the firm sought to frame the potential benefits of its proposal in similar terms. As described in the Board’s order, Canandaigua National argued that the proposed guarantee product would help customers of its bank subsidiary by enabling those customers to compete with other potential buyers who were capable of making all-cash offers. Canandaigua National also noted that “nonbank competitors” “already offer such products” in its market and argued the proposed activity would enable Canandaigua National and its bank to better compete with those nonbank participants.

By choosing to pass on conducting a Section 4(j)(2) analysis, the Board dodged having to offer a final conclusion on what it thought about the claimed benefits put forward by Canandaigua National. All the same, the Board’s statement about “concerns” that the benefits may be outweighed by negative effects, and the Board’s decision to name specific possible negative effects beyond those examples that are listed in the statute, give at least a hint as to how the Board thinks the analysis would have come out.

Does that mean the Board now in the complementary activities context will apply the Section 4(j)(2) factors differently from how it has previously applied them?

If so, some might welcome this outcome. And maybe the Board’s change in approach (if it is one) should have been expected, given that at one point people with these views appeared to have persuaded the Board that its original weighing of benefits and adverse effects had proven incorrect, at least in relation to certain activities.

The Board is reconsidering whether energy management services and energy tolling activities are complementary to a financial activity. … [T]he expected benefits of permitting these activities do not appear to have been realized over time. For example, it was originally expected that allowing FHCs to conduct energy management services and energy tolling activities would allow FHCs to gain additional information to help manage commodity-related risks. It is not clear that energy management services or energy tolling significantly improve an FHC’s understanding of commodity derivatives markets since—in order to engage in energy management services or energy tolling—an FHC must already have a thorough understanding of commodity derivatives markets. … The authorizations for energy management services and energy tolling also noted that unregulated financial competitors of FHCs engaged in these activities. However, it is unclear over time what, if any, advantages those financial firms gain from conducting energy management or energy tolling activities over FHCs in the conduct of derivatives and other FHC-permissible physical commodity activities.

A problem for the Board in adopting that argument here, however, is that the Board never finalized its 2016 proposal,16 at least in part because not all commenters agreed with the above assertions. This leaves things in a kind of odd place where the viewpoints reflected in the quote above were never officially adopted, and therefore at least based on the public record all of the Board’s previous physical commodities orders and their reasoning remain on the books.

So long as this is the state of play, the Board may at some point be required to more clearly explain just what it is that makes the balance of benefits and risks of physical commodity activities different from the balance of benefits and risks of guarantee programs like the one proposed here.

4. Was the Processing Timeline for This Application Consistent with the Law?

Once the Board “receives a complete notice” from an FHC of the FHC’s proposal to engage in a complementary activity, the BHC Act deems that proposal automatically approved unless the Board acts to deny the proposal within 60 days (subject to certain extensions).17

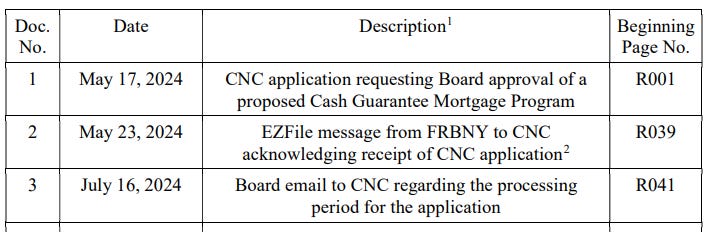

According to the order, Canandaigua National argued that the relevant time period had expired and therefore the Board no longer had authority to disapprove the proposal. The Board in the order rejected this argument in footnote 33, saying that “the Board considers the Notice complete as of April 22, 2025,” starting the 60-day clock, and that after taking into account the extensions the Board made thereafter, the ultimate action in October 2025 to disapprove the proposal was timely.

Notably not included in footnote 33 was the date when Canandaigua National initially submitted its proposal. The Board now in the Second Circuit litigation has filed a list of documents in the administrative record, and maybe you can see why the order chose to leave this date out.18

In plain terms, the May 17, 2024 initial filing date means it took more than 11 months after filing of the application for the Board to deem the application “complete,” and a total of 17 months for the Board to issue an 11-page final order denying the application.

Framing it as we have so far, this processing timeline seems faintly ridiculous, and suggests the Board may not have fully kicked its habit of dragging out action on applications it would prefer just go away.

On the other hand, there may be at least some evidence that the application may not have been ready for action when first filed. Canandaigua National’s original submission itself is not in the public record, but the list of documents in the administrative record indicates that, months after the original filing, Canandaigua National and the Reserve Bank were still trading emails regarding confidentiality, and that Canandaigua National ultimately had to resubmit some documents.

Rightly or wrongly, it took until mid-September to get that sorted out, and additional information requests were then sent to Canandaigua National on October 15, 2024; November 18, 2024; February 24, 2025; and April 11, 2025. The firm ultimately submitted its final responses to the requests on April 22, 2025, corresponding to the date cited in the order as the date on which the Board considered the application to be complete.

Do the above facts make the overall timeline more defensible? Maybe a little bit, although some of them raise their own questions, and ultimately without seeing any of the actual documents it is difficult to say.

Thanks for reading! Let us know what we got wrong at bankregblog@gmail.com

For citations to where to find these orders see footnotes 23-25 in the 2016 NPR.

As defined in the Board’s Wellpoint order in 2007.

The 2016 proposal also addressed conditions and requirements applicable to certain physical commodity activities conducted under other authorities under the BHC Act.

Because Canandaigua’s proposal is not in the public record, all factual descriptions in this post are based on, or quote directly from, the description of the proposal in the Board’s order denying the proposal.

The order states that Canandaigua provided examples of this happening when there were “changes in the circumstances of the customer between the preapproval and the time when final written approval would have been granted.”

The Board’s October 17 press release stated that a public order with the Board’s reasoning would follow after a review to ensure no inadvertent disclosure of confidential information. The public order was then published on November 20 via an update to the Board’s webpage with the original press release, without the Board issuing a new press release.

This is hardly a scandal, but the quiet approach the Board took here is different from the approach the Board took in 2023 with another rare application denial, when it in January issued a press release announcing the denial of the application, and then in March issued a new press release when the order was released.

See pages 7-8 of the order: “[T]he exception permitting national banks and bank holding companies to hold real estate acquired in satisfaction of debts previously contracted permits a national bank or bank holding company to hold real estate that was pledged to secure a credit extension, subject to certain maximum holding period requirements. In this way, national banks and bank holding companies reduce their credit risks. Under the proposal, by contrast, Canandaigua would be obligated to acquire the real property for its own account if it determines the proposed borrower is not creditworthy and therefore does not extend credit to the borrower.”

This letter is docket entry 3 in the Second Circuit litigation. The Canandaigua National request for reconsideration referenced in the Board’s letter is not publicly available.

Emphasis added. This quote comes from page 9 of the order, which states the Board’s conclusion on the safety and soundness factor and presumably therefore reflects a deliberate choice to use “and,” even though elsewhere in the order the Board uses language that tracks the “or” language in the statute.

The Board in previous complementary activities orders has imposed limits as percentages of capital, assets, and revenues. See for example the Board’s description of existing limits on physical commodities complementary activities in the 2016 NPR (“The Board placed certain restrictions on each complementary commodity activity … [T]he aggregate market value of commodities held under physical commodity trading and energy tolling may represent no more than 5 percent of the tier 1 capital of the FHC. The Board also imposed a cap on energy management services of no more than 5 percent of an FHC's consolidated operating revenues”). See also page 7 of the Board’s Wellpoint order (“[T]hese activities in the aggregate must not account for more than 2 percent of WellPoint’s consolidated total assets or 5 percent of its consolidated total annual revenues. In addition, the total assets of WellPoint’s subsidiaries engaged in disease management or mail-order pharmacy activities in the aggregate may not exceed 5 percent of the total capital … of all regulated insurance company subsidiaries and health plans of WellPoint.”)

The premise that Section 4(a)(2) prohibits most real estate activities is an accurate description of the end result, although it would be misleading to suggest, as the order sometimes comes close to doing, that the text of Section 4(a)(2) is uniquely or particularly focused on real estate activities. Section 4(a)(2) is a broad prohibition on nonbanking activities, related to real estate or otherwise, and is also subject to exceptions. The Board explains this in footnote 16 in the order, but its discussion elsewhere in the order loses some of that nuance.

Remember that in this context saying that Congress has not prohibited the Board from approving a complementary activity is not the same thing as saying that activity is necessarily permitted. To be permissible under Section 4(k)(1)(B) the activity still would need to be determined by the Board to be consistent with the statutory factors.

Emphasis added.

This description of physical commodity risks comes from the Board’s 2014 ANPR. See also the Board’s 2016 NPR (describing the risks associated with physical commodities activities as “unique and significant”).

Of course, the Board never adopted a final rule on physical commodities after issuing the 2016 proposal. So maybe you could resolve any perceived tension with the Canandaigua National order by saying, as some commenters did in response to the 2016 NPR and 2014 ANPR, that the Board was wrong to believe physical commodities risks were unique. If so, it could be reasonable for the Board to believe, as the Canandaigua National order necessarily implies, that physical commodity risks are actually more amenable to mitigation than risks relating to real estate.

It is one thing, though, for commenters on the 2014 ANPR and the 2016 proposal to think the Board got it wrong, and another thing for the Board to think it. If the Board now believes it was wrong in 2014 and 2016, shouldn’t it say so?

These quotes come from the 2003 Citigroup order, but the same potential benefits have generally been repeated in subsequent orders.

As recently as Spring 2024 the Board included plans to finalize the 2016 proposal in the long-term actions section of the Board’s submission of its unified regulatory agenda, the same place where the 2016 proposal had been listed on the regulatory agenda ever since the Fall 2017 version of the agenda.

See BHC Act Section 4(j)(1)(C) (general timeline of 60 days from receipt of complete notice); Section 4(j)(1)(C)(ii) (general right for Board to extend period by 30 days); Section 4(j)(1)(E) (right for Board to extend period for an additional 90 days in the case of, among other things, a proposed complementary activity that has not been previously approved by regulation).

The screenshot in the above post and the information discussed in the rest of this section comes from the certified list of the administrative record filed at docket entry 17 in the Second Circuit litigation.