Descending from the Summit

Descending from the Summit

The Fed enforcement action with Mode Eleven

Hulett is a town of a little more than 300 people located a few miles away from the Devils Tower National Monument in the Black Hills of northeastern Wyoming.

In downtown Hulett visitors will find a bank with a sign in the window saying, HOWDY. This bank, now called Summit National Bank, was founded in 1984 with the mission of “creating and building the basic infrastructure” the community needed to “fight the challenges that all small towns across the country were seeing.”

A BaaS Enabler

Skipping over the ups and downs of the intervening years, at some point a few years ago the bank and its parent company, Hulett Bancorp, decided to supplement their community banking activities1 with a new initiative.

In this new initiative, Hulett Bancorp, now doing business as Mode Eleven, embraced a role it would later describe as that of a “Banking-as-a-Service enabler that owns a national bank.” The BaaS page on the company’s website said:

When it comes to introducing new services, FinTechs and brands offering embedded finance have never been short on challenges. Regulatory issues and the limitations of core technologies have left many banks unable to fully respond to those needs.

As a result, innovation has often been slow or unsuccessful. At Mode Eleven, we believe it doesn’t have to be this way. And we’re here to change things.

Mode Eleven continued:

Banking is one of the mostly highly regulated industries in the world. For example, offering and supporting a prepaid banking product requires adherence to a challenging and cumbersome list of oversight requirements. Mode Eleven technologies and processes give you a market-ready, compliant solution.

A slide deck from August 2022 lists various capabilities, including “lending-as-a-service,” “deposits and branded accounts,” “access to payment rails,” “digital asset custody” and “compliance management.”

OCC Conditional Approval of Substantial Change in Assets

That same slide deck also describes the OCC as having “approve[d]” Summit National Bank’s “BaaS business strategy.” That is not exactly how I would describe what happened, but the OCC did in February 2022 conditionally approve an expansion of the bank’s operations to include what the OCC described generically as “a new FinTech Division in which traditional banking products and services will be offered to FinTech-sourced customers.”

The OCC’s approval was conditioned on Summit National Bank developing and adopting (and then receiving no supervisory objection to) an appropriate third-party risk management program.

Nexo Acquires an Unspecified Stake

In September 2022, the crypto lending and borrowing platform Nexo announced that it had made a “transformative deal” to acquire a stake in Mode Eleven.2 The “industry-changing transaction” would “further boost” the company’s U.S. presence, and would enable Nexo clients to “open bank accounts with Summit National Bank, as well as enhanced lending and card products, utilizing its decades-long track record of excellence in regulatory compliance and the existing infrastructure.”

The exact size of the stake Nexo acquired through its transformative and industry-changing acquisition has never been clear. Based on publicly available information, no application was ever filed with the Federal Reserve Board under either the Bank Holding Company Act or the Change in Bank Control Act.

Nor is it clear whether Nexo continues to hold any interest in Mode Eleven. Just a few months after announcing the Mode Eleven investment, Nexo in early December 2022 said that it had made the “regrettable but necessary decision” to phase out its products in the United States, and therefore intended to make a “gradual departure” from doing business there. As Nexo explained in its press release, this announcement came in the shadow of various investigations by the SEC, CFPB and state securities regulators.3

Financial Results

Many banks that have embraced fintech growth strategies have experienced rapid (often in the eyes of regulators, too rapid) growth in asset size and deposit base. You can sort of see that with Summit National Bank as well, although there is significant quarter-over-quarter variation.4 The bank has also recently begun to rely on brokered deposits as a source of funding.5

In 2023, Summit National Bank reported a net loss of $1.37 million, following a loss of $213,000 in 2022. At the parent company level, Mode Eleven reported a net loss of a little over $6 million for 2023, after reporting a net loss of over $5 million for 2022.

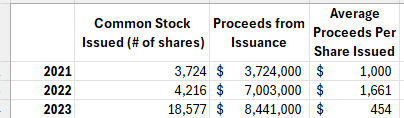

The parent company financial statements for 2021, 2022 and 2023 filed by Mode Eleven with the Federal Reserve Board also report that the company issued new common stock in each of those years:6

The parent company financial statements are not required to, and do not, explain who the shares were issued to, whether they are voting or non-voting, or other things that may be relevant from a regulatory perspective.

Federal Reserve Board Enforcement Action

Last Thursday, the Federal Reserve Board published a cease and desist consent order it entered into with Mode Eleven Bancorp in late March.

The consent order begins by observing that Mode Eleven had adopted a “fintech business strategy,” which the order defines as “a strategy focused on providing banking-related services to financial technology companies through certain nonbank subsidiaries.”7 The order also notes that this strategy “requir[ed] significant financial and managerial resources and support from” Mode Eleven.

According to the order, an examination by the Federal Reserve Bank of Kansas City that wrapped up in 2023 identified multiple deficiencies in Mode Eleven’s operations, “including with respect to pursuit of the fintech business strategy, related to board oversight, capital, earnings, liquidity, risk management, and compliance with the rules related to affiliate transactions.”

Mode Eleven is therefore required to take various actions to strengthen board oversight and risk management, to better manage liquidity and capital, and to otherwise improve operations.

With respect to the fintech initiative, the order says that Mode Eleven has already “voluntarily ceased pursuit of the fintech business strategy and is winding down all related activities.”

To ensure that Mode Eleven follows through on this, paragraph 11 of the consent order requires that Mode Eleven immediately cease from engaging in “any expansionary activities related to the fintech business strategy, including the establishment of any new subsidiaries, business lines, products, programs, services, customers, or program managers in connection with the fintech business strategy, without the prior written approval of the Reserve Bank.”

Paragraph 11 also requires that Mode Eleven provide the Reserve Bank with a complete summary of all costs and expenses incurred to exit or wind down the fintech business strategy, along with a plan setting out the timeline and process for completing the winddown and paying any remaining costs or creditors.

Change in Bank Control Act Compliance

The provisions of the consent order discussed above are more or less consistent with the growing catalogue of other BaaS- and fintech-related enforcement actions brought recently by the Board, FDIC and OCC.

Paragraph 12 of the consent order is a little different. The paragraph begins by saying that Mode Eleven must strengthen and maintain its internal controls to “ensure that ownership interests in [Mode Eleven] are properly identified and aggregated in compliance with the requirements of section 225.41 of Regulation Y.” This is a reference to the provision of the Federal Reserve Board’s Change in Bank Control Act regulations which requires prior notice (and effectively prior Board approval) of certain acquisitions of shares in a bank holding company, like Mode Eleven.

Paragraph 12 goes on to require Mode Eleven to keep better track of the following information:

Whether any investor owns or controls, directly or indirectly, 5% or more of any class of Mode Eleven’s voting securities, or of its total committed capital, including:

aggregated shareholding information for investors acting in concert or that are commonly controlled;

identification of any business or family relationships presumed under the regulations to indicate that persons are acting in concert;

identification of any person that serves as a general partner, manager, managing member, investment adviser, or person acting in a similar capacity, at any legal entity presumed under the regulations to exercise control over Mode Eleven;

contact information and corporate registration information for non-U.S. legal entities owning an interest in Mode Eleven;

The source of funds used for each shareholder’s purchase of their interest in Mode Eleven; and

any agreement, formal or informal, between an investor in Mode Eleven and any other shareholder of Mode Eleven relating to the investor’s purchase of Mode Eleven shares.

The consent order does not offer any explanation for why paragraph 12 was included, so it is not clear if something happened in relation to a previous investment that raised the Board and Reserve Bank’s concerns, or whether this is a more prophylactic measure.

Summit National Bank has consistently achieved Outstanding CRA performance ratings dating back to 2004, with the OCC’s most recent performance evaluation finding that the bank’s lending activity “reflect[ed] excellent dispersion among businesses and farms of different sizes in all AAs” and that the bank’s community development activities “reflect favorably on the institution’s responsiveness to community development needs, especially in light of the economic disruptions caused by the COVID-19 pandemic.”

Throughout this section, the post assumes that the September 2022 Nexo press release marked the closing of the investment, rather than the signing of an agreement that, subject to certain conditions, would result in the investment. I think that is the best way to read things, but the press release is never completely clear on this or other points.

In January 2023 the SEC announced that Nexo had agreed to pay a $45 million penalty (half to the SEC and half to state regulators) related to the unregistered offering and sale of a retail crypto asset lending product.

Information in the table comes from the bank’s call reports (RSSD ID 78559).

Or, alternatively, the bank’s funding sources have stayed the same, but some of those same funding sources are now classified as brokered deposits.

Information in this table comes from Schedule SC, Item 16.b and the notes to the financial statements on the very last page of the parent only financial statements linked above. In addition to the common stock issuances listed here, in 2021 Mode Eleven also issued 5,727 shares of preferred stock, raising $143,000 in proceeds.

It is not clear which nonbank subsidiaries the order has in mind here — Mode Eleven’s FFIEC org hierarchy lists no subsidiaries of the company other than Summit National Bank.

This comes up again later in paragraph 10 of the consent order, which says that Mode Eleven must take action to ensure that Summit National Bank complies with the affiliate transaction restrictions of Section 23A/23B and Reg W, “in all transactions between the Bank and its affiliates, including, but not limited to, Bancorp and its nonbank subsidiaries.”

Even assuming the FFIEC org hierarchy is up to date, it is sourced from a reporting form with a definition of subsidiary that is sometimes different from the definition of subsidiary that applies in various Board regulations, so this is not to say that the order is necessarily wrong when it talks about nonbank subsidiaries. (Or this is just form language intended to cover any nonbank subsidiaries the company might establish in the future.)