A Few Bank Regulatory Notes on Banc of California-PacWest

Also, the failure of a small Kansas bank

Something I used to think about a lot is an article Matt Levine wrote a long time ago highlighting an academic paper by Jeffrey Manns and Robert Anderson IV called The Merger Agreement Myth. From the authors’ abstract:

[W]e designed a modified event study to test whether markets respond to the details of the legal terms of acquisition agreements. Our approach leverages the fact that merger announcements (which lay out the financial terms) are generally disclosed one to four trading days before the disclosure of acquisition agreements (which delineate the legal terms). […] Our analysis shows that there is no economically consequential market reaction to the disclosure of the details of the acquisition agreement.

As Levine writes, depending on your line of work that finding might fill you with “either very mild amusement or CRUSHING EXISTENTIAL DESPAIR.”

I was always more in the mild amusement camp, but in any case because this post discusses the Banc of California - PacWest transaction documents filed by the parties with the SEC yesterday before EDGAR closed for the weekend, I thought it was worth highlighting this point up front just to make clear that I am not saying any of what follows truly matters or moves the needle on the conclusions the markets have already drawn re: the deal.

That caveat acknowledged, the transaction documents do include a few interesting bank regulatory provisions, so let’s discuss them here.

Opting for Federal Reserve Supervision

Banc of California’s depository institution subsidiary, Banc of California, National Association is currently a national bank supervised by the OCC. PacWest’s depository institution subsidiary, Pacific Western Bank, is a California-chartered nonmember bank supervised by the FDIC.

As disclosed by the parties in their merger press release, Banc of California, N.A. will merge into Pacific Western Bank, with Pacific Western Bank surviving (but taking on Banc of California’s name). Before doing that, though, Pacific Western Bank will apply to become a member of the Federal Reserve System, such that formal FDIC approval would not be required for the bank merger and that after the transaction closes the bank would be supervised by the Federal Reserve Board (and the Federal Reserve Bank of San Francisco under delegated authority).

This is Section 1.15 of the Merger Agreement.1

Efforts to Obtain Regulatory Approvals

As is pretty standard, the parties agree to use reasonable best efforts to close the merger, including by resolving any objections asserted by a governmental entity, provided that neither party shall be required to agree to a Materially Burdensome Regulatory Condition.

The specific definition of that term, though, is interesting and a little different to what I recall seeing before in other large public company bank M&A deals. Specifically, the parties are not required to agree to anything that would:

require the issuance of additional equity or other capital in excess of the amount contemplated by the parties in the agreed equity financing; or

subject the surviving company to regulatory standards that (i) “do not apply to a similarly sized financial holding company and state member bank that are well-capitalized and well-managed” and (ii) are “materially more burdensome, individually or in the aggregate, on the operations, business or profitability” of the surviving company than those currently applicable to Banc of California.

This is Section 6.1(c) of the merger agreement.2

(Note also that the agreement contemplates using reasonable best efforts to file all required regulatory applications by August 14 at 5:30 p.m. See Section 6.1(b).)

MAE Definition Reference to Wholesale Funding and CET1 Capital

The agreement gives Banc of California the right to terminate the agreement if there is a material adverse effect on PacWest and likewise gives PacWest the right to terminate if there is a material adverse effect on Banc of California.

This again is typical, but the specific definitions of MAE in this context are sort of interesting. In particular, the respective MAE definitions are tied to, among other things, a party’s regulatory capital and its amount of wholesale funding.

[MAE means,] with respect to PACW, (1) PACW’s Net Wholesale Funding Amount as of the Measurement Time is at least one billion seven hundred and fifty million dollars ($1,750,000,000) greater than the PACW Reference Net Wholesale Funding Amount, (2) as of the Measurement Time, the common equity Tier 1 Capital (as defined in 12 C.F.R. 217.20) of PACW is less than the amount set forth in Section 3.1(a) of the PACW Disclosure Schedule […]

[MAE means,] with respect to BANC, (1) BANC’s Net Wholesale Funding Amount as of the Measurement Time is at least one billion seven hundred and fifty million dollars ($1,750,000,000) greater than the BANC Reference Net Wholesale Funding Amount, (2) as of the Measurement Time, the common equity Tier 1 Capital (as defined in 12 C.F.R. 217.20) of BANC is less than the amount set forth in Section 3.1(a) of the BANC Disclosure Schedule, except as a result of the matters set forth in Section 3.1(a) of the BANC Disclosure Schedule […]

These definitions are from Section 3.1 of the merger agreement. As is standard, the disclosure schedules are not filed publicly.

Investment Agreements

A key feature of the transaction is the parties having lined up a total of $400 million in new equity from Warburg Pincus and Centerbridge.

The investment agreements with Warburg and Centerbridge include the typical set of bank regulatory provisions intended to make sure the parties are not deemed to have control for bank regulatory purposes.

Oral Confirmation of Non Control

Further to that end, each agreement also conditions closing on its respective purchaser having “received reasonably satisfactory oral confirmation from staff of the legal division of the Federal Reserve that the consummation of the Closing will not result in Purchaser being deemed to have, or have acquired, ‘control’…”3

Efforts to Close

The investment agreements also contain a definition of Materially Burdensome Condition - i.e., a list of things the private equity investors cannot be required to do in order to close the investment. These include:4

controlling Banc of California or being required to become a BHC under the BHC Act;

controlling Banc of California or being required to provide prior notice under the CIBC Act;

serving as a source of financial strength to Banc of California; or

entering into any capital or liquidity maintenance agreement or any similar agreement with any governmental entity, providing capital support to Banc of California, PacWest, or their subsidiaries, or otherwise committing to or contributing any additional capital to, providing other funds to, or making any other investment in, Banc of California, PacWest or their subsidiaries.

The Specified Person

The Centerbridge agreement includes a standard representation that Centerbridge is not acting in concert (as defined under Regulation Y) with any other person in connection with the transactions.

The Warburg agreement has the same sort of provision, but includes the caveat “Other than the Specified Person…” Specified Person is defined as “any person set forth on Section 4.2(c)(iv) of the Company Disclosure Schedule.”5

Heartland Tri-State Bank Fails

Last night the FDIC announced that it had been appointed as receiver of Heartland Tri-State Bank of Elkhart, Kansas6 and that Dream First Bank, National Association of Syracuse, Kansas had agreed to assume all of the failed bank’s deposits.

In its own separate announcement, the Kansas Office of the State Bank Commissioner said that it had “determined that Heartland Tri-State Bank was insolvent” and therefore had taken charge of the properties and assets of the bank. The OSBC did not specify what exactly happened, other than to say that “Heartland Tri-State Bank became insolvent due to an isolated event” and that the overall Kansas banking industry should be unaffected and remain strong.

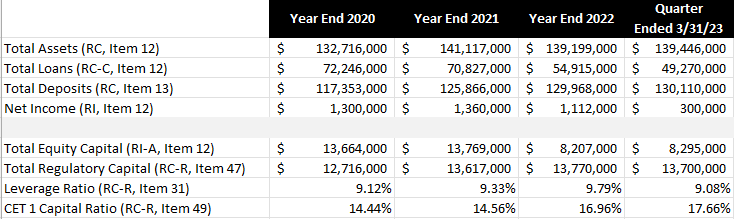

I hope we learn more details about what happened here. Obviously one’s mind immediately goes to the interest rate risk issues that were highlighted by the banking stress of earlier this year, but a superficial look at Heartland Tri-State Bank’s call reports, a few key items of which are highlighted below, does not to me definitively make that case.7

One other thing that may well be irrelevant but that nonetheless makes this interesting: As Claire Williams of the American Banker noted last night, Heartland Tri-State Bank’s CEO until recently served as chair of the Kansas Bankers Association, and has been a prominent advocate for rural and community banks, testifying before Congress and serving on various advisory committees.

In detail:

FRS Membership and Bank Merger. Promptly following the Second Effective Time, Pacific Western Bank, a California-chartered non-member bank and, prior to the Second Effective Time, a wholly-owned Subsidiary of PACW (“Pacific Western Bank”), shall become a member bank of the Federal Reserve System (the “FRS Membership”). Promptly following the effectiveness of the FRS Membership, Banc of California, National Association, a national banking association and a wholly-owned Subsidiary of BANC (“Banc of California”), shall merge with and into Pacific Western Bank (the “Bank Merger”). Pacific Western Bank shall be the surviving entity in the Bank Merger (the “Surviving Bank”) and, following the Bank Merger, the separate corporate existence of Banc of California shall cease. […]

In detail:

Each party shall use its reasonable best efforts to respond to any request for information and to resolve any objection that may be asserted by any Governmental Entity with respect to this Agreement or the transactions contemplated hereby in each case in a reasonably prompt and timely matter. Notwithstanding anything in this Agreement to the contrary, neither BANC nor PACW nor any of their respective Subsidiaries shall be required (and without the written consent of the other party, neither BANC nor PACW nor any of their respective Subsidiaries shall be permitted) to take any action, or commit to take or refrain from taking any action, or agree to any condition or restriction, in connection with obtaining the foregoing permits, authorizations, consents, Orders or approvals of Governmental Entities that would (i) reasonably be expected to require the Surviving Corporation or any other person to issue equity securities or otherwise raise capital in excess of the amount contemplated by the Equity Financing; or (ii) (A) not apply to a similarly sized financial holding company and state member bank that are well-capitalized and well-managed and (B) be materially more burdensome, individually or in the aggregate, on the operations, business or profitability of the Surviving Corporation and its Subsidiaries than those imposed on BANC or Banc of California as of the date of hereof (each of clauses (i) and (ii), a “Materially Burdensome Regulatory Condition”). Any requirement to enter into any BSR Agreement or otherwise take actions contemplated by Section 6.21 shall not be a Materially Burdensome Regulatory Condition hereunder.

This is Section 1.2(b)(2) of the Centerbridge agreement and Section 1.2(b)(3) of the Warburg agreement.

This is Section 4.4 of the Centerbridge agreement and Section 4.7 of the Warburg agreement.

See Sections 2.3(i)(ii) and 4.2(c)(iv) of the Warburg agreement.

Heartland Tri-State Bank was a Kansas-chartered state member bank, having converted from an OCC charter in 2017.

You can see the effect of AOCI in the decrease in total equity capital (but not regulatory capital, because the bank had an AOCI opt-out election in place) but even taking this into account that doesn’t seem to me to be enough to explain the bank’s apparent insolvency.

That said, this sort of analysis of community bank financial statements is well outside my wheelhouse, so of course please do write in and yell at me to say that no, actually one or more things in the call reports in fact should have been a screaming warning sign.